Introduction:

- Choosing between renting and buying a home is a big decision and the best option for you will depend on a number of factors.

- Factors including your finances, lifestyle, and future plans. In this post , we’re going to look at renting versus buying.

- Things like property value, taxes, maintenance, and repairs, and some questions to ask yourself to help you weigh your options when it comes to renting.

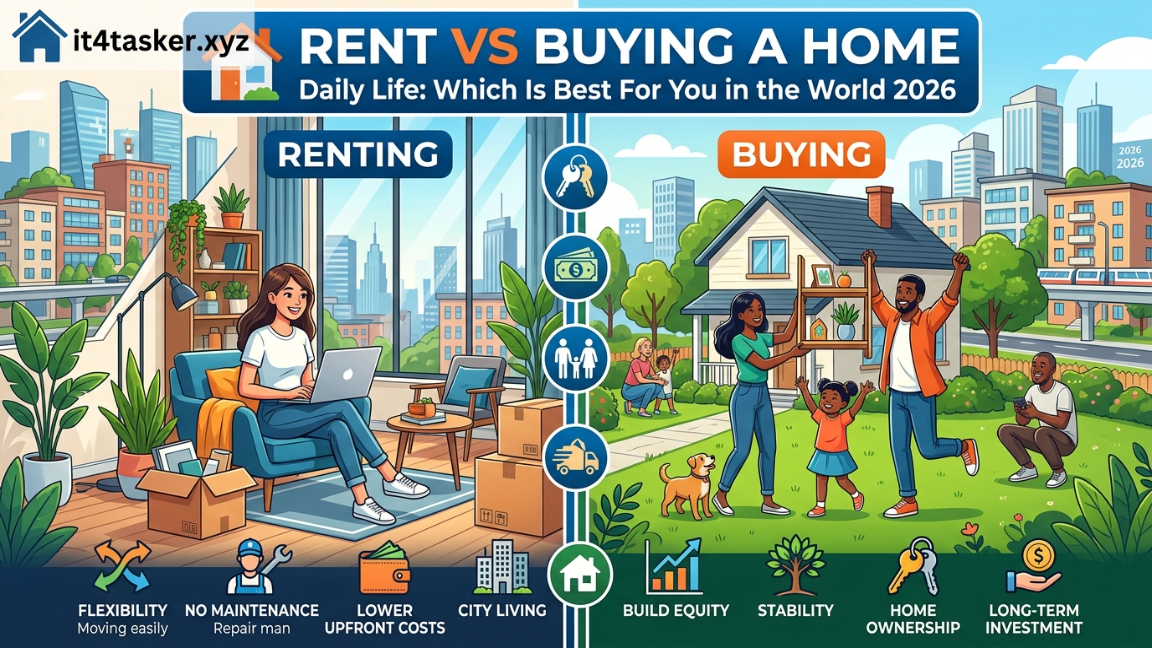

The Case for Renting:

- While home ownership holds a certain something.

- Renting comes with a whole box of benefits that are often overshadowed.

- Traditional ownership is better off painting a new narrative that clearly shows why renting can be a good fit.

- Your perfect fit Consider yourself first.

- Financial strength Personal investment Think about dropping $220,000.

- Paying down a condo and investing instead It’s in that business you’ve always dreamed of starting or being able to start Paying that money aggressively Renting lets you invest.

- Give yourself your emotions and your wallet Not just breaking the brick-and-mortar location

- Freedom you don’t even want Your home to determine your destiny if you land Your dream job in a bustling city Country rental allows you to pack.

- Chase your bags and this opportunity.

- Without the headache of selling a house Or you decide to test the waters in a.

- A vibrant city apartment for a year Before committing to buying in Suburban location freedom empowers.

- You don’t just have to live life on your own terms.

- Your property terms time and Maintenance freedom time is your most valuable.

- You can rent out valuable resources.

- You spend it wisely on those faucets that can bother you for weeks.

- Endless weekends spent trimming overgrown.

- Backyards as a renter you just dial.

- You have a landlord and they set it up by number.

- Unexpected maintenance bills or Property tax increases are your loss Carefully crafted budget so you can Spend this Saturday afternoon catching up.

- Take a walk with your favorite read.

- Friends or relax instead.

- Trying to fix a plumbing problem in your time.

- Again it’s yours to decide what you can prioritize.

- Really adds flexibility to your life.

- Renting lets you downsize from a.

- Spacious family home to a cozy studio Apartment after your kids go College or you can easily upgrade.

- From a one bedroom apartment To a three bedroom townhouse as your family Expands without the hassle and expense.

- Allows for renting to sell and buy.

- To take the hassle out of home ownership And focus on enjoying your life.

- Not burdened by the issue of rent to buy.

The Case For Buying:

- It gives you freedom but buying a home gives you.

- You strengthen your community and can help.

- You reach the definition of financial freedom.

- Perhaps the biggest vote for ownership is the definition.

- Close your eyes and see yourself 10 years from now with your weird starter home having increased in value thanks to the rising market trends and your careful maintenance of a $200,000 mortgage.

- Ready for a $300,000 Nest Egg.

- Fund your retirement dreams or your children’s.

- College education By now you can tell.

- That owning your home is not just about a roof over your head.

- It’s a potential.

- Unlike rent that disappears into the landlord’s pocket. Every mortgage payment becomes Foundation of your personal wealth Dream when you channel an additional.

- Money for your mortgage that you know you have.

- You are building a home with equity tax benefits.

- Ownership also comes with tax benefits.

- From mortgage interest deductions to property tax credits that you get to reduce your taxable income and receive a Leave you with more money to invest come tax season Your home grants you the freedom to transform it into a.

- It reflects your unique style.

- The canvas where your dreams take clear shape.

- You can tear down that cluttered wall.

- And create an open-concept living space You will be bathed in sunlight.

- The satisfaction of retreating and Appreciating your hard work

- You have replaced the lush garden.

- Your nurturing and comfortable reading nook.

- You have made the community more like a rental.

- Allows freedom and flexibility.

- Some may find moving around more nomadic.

- Stressed existence allows you to.

- Put down roots in the community you love.

- Watch your children grow up within it

- Build and create the familiar walls of your home

- Lasting traditions that become.

- The fabric of your family history before us

- Get a couple of extras

- Consider when deciding between renting.

- And if you’ve enjoyed the video so far, owner

- Please consider liking and

- bookmarking my website to this really helps us now.

- Let’s talk about the three biggest.

- Factors between choosing and Three questions you should ask yourself.

Property Value:

- The value of a property when it comes to renting.

- And the difference between buying a property

- Value is perhaps the most fundamental.

- The aspect to consider as a tenant

- You have no ownership stake in the property.

- There are no fluctuations in its value

- that directly affect you financially.

- Rent can increase over time based on

- Market factors and lease terms but this

- is not tied to the proper property

- Intrinsic value but your

- mortgage payments as a homeowner contribute to the building.

- Over time, the equity in the property

- If the value of the property increases your standing.

- When you sell it, you can financially

- Gain.

- Become a significant source of wealth.

- Especially stable and accumulated in

- During appreciating markets

- The potential for appreciation is attractive.

- It also carries a risk of depreciation.

- If you need to sell in a falling market, the thing about property value is that it can potentially replace your mortgage.

- The payment, but the rent, usually remains.

- At least within the terms of the lease, stable monthly expenses and easy taxes are not included in the budget.

- Tenants are responsible for paying property taxes, which are imposed by local governments.

- The assessed value of the property can be a significant cost savings, especially in areas with high property taxes.

- They cannot deduct mortgage interest or property taxes, but they can.

- Depending on their income and rental situation, they may be eligible for a tenant tax credit. Credits that can be offered directly to the tax payer.

- Homeowners, on the other hand, are fully responsible for paying the annual property tax.

- The costs and rates can vary greatly. Depending on the location, they can. Reduce their interest.

- Mortgages from their taxable income Potentially reducing their tax liability That can be especially beneficial for.

- Those with high mortgages can also.

- But are eligible for depreciation.

- Property can further deduct these

- Reduce their overall tax burden.

Maintenance and repairs:

- When it comes to maintenance and repairs.

- Maintenance and repairs are usually

- the landlord’s responsibility to fix.

- Major appliances, plumbing issues, structural issues, and other necessary

- repairs can give the tenant peace of mind.

- Knowing that they won’t be burdened by it.

- Unexpected repair costs, on the other hand, are something that tenants have limited control over.

- Repairs and renovations can be made by landlords.

- Prioritize functionality over aesthetics.

- And may not be worth making major changes

- unless they add to the value of the property.

- As the homeowner, you are responsible for them.

- All of this can be expensive and time-consuming

- and requires a budget.

- Repairs and potential repairs are, but

- homeowners have full control.

- Their property allows them to make

- repairs and renovations as they see fit.

- Giving more personalization and

- satisfaction with the living space now

- is more important to determine who is best for

- You and your unique individual need to ask yourself these three questions:

How long will you stay?

- I will be there as long as you know.

- The potential time frame in a place is the most important factor in deciding between renting and buying, like deciding whether to rent a bike.

- Buying one for a short-term trip to the park or an investment Are you living there for a short term like 1?

- Mid-term 3 to 5 years or long-term 5 plus years If you see yourself staying for just a couple of years, a rental offer is unmatched.

- Flexible moving to a new job, pursuing temporary opportunities or navigating life changes goes a long way.

- Easy to sell without the burden of down payments, realtor fees, and potential market costs.

- These costs can fluctuate over a short time frame.

- Renting still offers the benefits of ownership, but buying becomes more expensive.

- If you find yourself in the same place for years, equity building accelerates. Potential appreciation offers financial rewards.

- Profits and mortgage payments over time are often more stable than renting.

- You have control over your living space and can customize it to your heart’s content.

- I’ve saved two for your peace of mind.

Have you saved enough?

- Buying a home is a significant financial milestone that requires a healthy dose of careful planning and the fact that you have saved enough.

- A yes or no question of affordability, lifestyle choices, and long-term desires are all in question while many associate saving enough with a down payment.

- A down payment is included in home ownership.

- Other expenses, including closing costs, can range anywhere from 3 to 6 percent. The purchase price, monthly mortgage payments, of course, are the headliners.

- But don’t forget other expenses like property taxes, PMI, homeowners’ insurance, and HOA fees and maintenance during your move.

- You don’t have to be your own handyman.

- You want a strong emergency fund to anticipate and handle unexpected maintenance and repairs.

Can you afford it?

- While for many people a dream comes with a hefty price tag and ongoing financial commitments, it’s important to take a deep dive before jumping into the deep end.

- Ask yourself some key questions that will help you decide what you want to do.

- Compare your monthly mortgage payments to your total income, including the mortgage. Ideally, keep your DTI to less than 36%. A higher DTI can leave you financially stressed and struggling to keep up with ongoing expenses.

- Another key number you need to consider is your emergency fund.

- Your emergency fund should ideally cover 3 to 6 months of living expenses.

- There should be no unexpected repairs or job loss.

- Consider your financial security.

- Your current savings and any potential investments that could bring in.

- In the additional income you can allocate a.

- Their share towards home ownership Without jeopardizing your long-term Financial goals so if stability and Expected expenses are key rent.

- May be a better option that you avoid.

- Risk of market fluctuations and Unexpected expenses while maintaining Flexibility and freedom of movement However if you have savings Build equity and can see yourself there.

- Can buy for a long period of time

- Being a great option Thank you very much.